With a more carefully designed property tax system, local (property) tax revenues could be increased by approximately 10–15 percent even without raising tax rates. Based on the findings of its audits initiated in 2024 covering the property taxation practices of around 20 local governments, the State Audit Office of Hungary has formulated a number of constructive recommendations to support more efficient tax collection.

For a municipality, local tax revenue can provide a significant source of development funding, the basic prerequisite of which is the existence of a tax policy tailored to local conditions, the tax-paying capacity of resident or locally operating taxpayers, and municipal objectives.

Although the local business tax is the largest source of revenue among local taxes (generating HUF 1,348.6 billion in 2024), local governments may also decide in their tax decrees to introduce various local (property) taxes (such as the building tax, the land tax, and communal tax on private individuals). In 2024, approximately two-thirds of municipalities operated one or more types of local property tax, generating HUF 225.2 billion in revenue. The majority of this revenue – 77.2 percent – came from the building tax, primarily levied on non-residential buildings.

One of the most sensitive issues in local taxation in Hungary is property tax: there is a deep-rooted socio-cultural resistance to the taxation of real estate in Hungarian society, which is why local governments bear a particularly heavy responsibility in this regard.

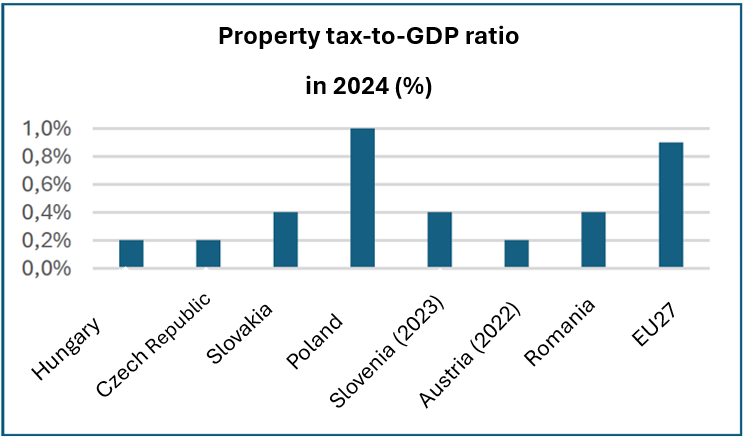

At the same time, in the field of property taxation, local governments currently have considerable autonomy – even in international comparison – both in setting tax rates and in designing exemption schemes. The ratio of property tax revenues to GDP does not differ significantly from regional patterns, although it is significantly lower compared to the EU average.

According to the State Audit Office of Hungary (SAO), without raising the tax rate, it is possible – based on their estimates – to increase local (property) tax revenues by approximately 10-15 percent simply through more efficient property taxation (without increasing the amount of the solidarity contribution payable).

However, this requires, on the one hand, local property tax regulations aligned with local conditions, municipal and tax policy objectives, and higher-level legislation, and, on the other hand, a tax authority with the appropriate competence and capacity to enforce tax rules.

To facilitate all of this, based on its findings of the audit on municipal property taxation, the SAO issued non-binding, constructive proposals worth considering to the relevant stakeholders (local governments, clerks, competent ministers, and the Hungarian State Treasury), aimed at improving the efficiency of local property taxation.

Clear tax policy objectives and tax regulations that are consistent with the law and aligned with those objectives

Among the proposals formulated within the framework of more sound local regulations that makes full use of available opportunities, the primary point is that a coherent tax decree – one that complies with statutory provisions and reflects the will of the local government – can be optimally established only if the municipality has a clear set of tax policy objectives and concept that aligns with the operational needs of municipal public services and the municipality’s development goals.

In the course of its development, it shall not be disregarded that local government tax policy shall reflect the geographical, economic, sociological, and social characteristics of the municipality, as well as the tax-paying capacity of the taxpayers.

Tax regulations designed in accordance with these criteria shall be reviewed on an ongoing basis, both to keep pace with changes in the legal provisions relevant to local taxation and to ensure that they remain consistent with local tax policy and local economic conditions.

More efficient and entirely lawful tax collection

According to the position of the SAO, adequate and continuously developed professional competence is essential for the efficient and lawful performance of tax authority duties. To support this, regular professional training should be provided to local government tax authority staff, as well as to government office staff acting in a second-instance tax authority capacity over them.

The identification and detection of taxable properties shall play an important role in the task performance of efficient tax authorities. To carry out these tasks, the regular use of digital tools (satellite imagery, aerial photography, street view imagery, and orthophotos) is recommended.

It is also an important requirement that the tax authority decisions are lawful, properly reasoned, and understandable. This can reduce the time spent handling taxpayer complaints and appeals. Tax assessment decisions and other documents relevant to taxation (e.g., data reports, acknowledgments of receipt) shall be retained for as long as any legal effect is attached to them; therefore, premature disposal shall be avoided.

Efficient tax assessment should be complemented by rapid and prompt tax enforcement. This is necessary not only to increase revenue, but also to demonstrate support for taxpayers who comply with the law, i.e. those who pay on time.

According to the professional assessment of the SAO, issuing a payment reminder after 30 days of arrears and initiating enforcement measures after 60 days of arrears would be an efficient tool for collecting tax debts.

Reforming the legal framework for property taxation to ensure efficient taxation

According to the auditors of the SAO, it should be considered whether the legal framework could enable the implementation of tax enforcement and tax auditing in an association-based form. This is particularly relevant given that the proper performance of specialized tax authority tasks (such as tax audits and tax enforcement) require specialized expertise and practical experience, which may not necessarily be worth developing in every small municipality.

In addition, the State Audit Office of Hungary raised the possibility that one tool for more efficiently preventing either multiple taxation or the failure to levy taxes could be reducing the number of taxes and the complexity of tax administration, i.e. simplifying the technical aspects of tax legislation. It may be possible to apply a codification approach that does not substantially change the right of municipalities to set taxes.

Development of the Hungarian State Treasury’s specialized system

The ASP.ADO specialized system could more effectively support the identification of taxable items and taxpayers if it enabled the automatic extraction of potential taxable items and taxpayers that are not included in the data provided annually by the real estate authority or are not recorded in accordance with the real estate registry.

It would also assist the tax authorities in their tax assessment tasks if the Hungarian State Treasury periodically (at least annually) substantively reviewed, updated, and expanded the sample decisions used in its tax registry software that it operates.

Conclusion

Overall, in order to make local taxation more efficient, according to the position of the auditors of the SAO, both a slight modification of the existing legal framework, a reconsideration of local tax policy, and an improvement in the efficiency (and in some cases capacity) of municipal tax administration can be appropriate tools.

It should also be emphasized, however, that constructive recommendations are not binding on the recipients; rather, they are intended solely to help make the best possible use of the potential opportunities inherent in local taxation, taking into account considerations of efficiency, cost-effectiveness, and practicality.

The full analysis is available in Hungarian here.

The authors of the professional article underlying the original summary are: Gabriella Baffia-Klement, auditor; Dr. Zsófia Heizer-Kiss, senior auditor; Dr. Anikó Farkas Nagyné, auditor; and Lóránd Kanyó audit manager